The consequences of rise in oil prices and the war in Ukraine on African economies

Russia's invasion of Ukraine is a major crisis that will have long-term consequences for the entire planet. It comes as Africa struggles to put its economy on the path to recovery, amid continued pandemic, global inflationary pressures and financial and commodity market volatility. Some energy-exporting countries will be able, to varying degrees, to bernefit from the crisis. But the vast majority of countries, all net energy importers, are already hard hit by soaring energy and food prices. These disruptions will accentuate their external imbalances and heighten their concerns about rising prices, the evolution of public debt, and, more generally, their position in the new geopolitical context.

The economic situation at the start of the conflict (February 2022)

The international situation

The current situation is particularly difficult. The global economy is admittedly in its second year of recovery and the World Bank's Economic Outlook forecasts growth of 4.4% in 2022. But uncertainty remains high due to the continuation of the pandemic, the price surge and the threat of increasing interest rates. In most industrialized countries, inflation already exceeds 5% year-on-year (early 2022 compared to early 2021). In the United States, prices rose by 7.5% in January 2022 and the Fed plans several increases in its key rate in 2022 and 2023. In certain more fragile countries, the inflation rate is even much higher (+15.7% in Nigeria).

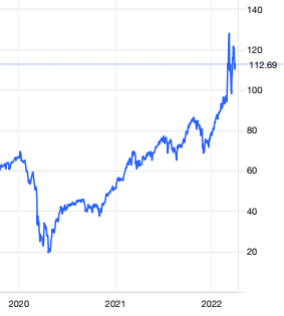

The rise in the price of crude oil comes in an already difficult context. Indeed, contrary to a widespread idea, the price hike does not find its origin in the war in Ukraine. In fact, the price of crude oil has been on an upward trend for two years. Following the collapse in the spring of 2020, caused by the first lockdown measures and the slowdown in global economic activity, Brent had risen from $20 in April 2020 to $63 a year later, and it already reached $95 on the 22nd. February 2022, on the eve of the invasion. The war and the uncertainties it creates have naturally amplified the phenomenon: at over $100 per barrel, the world price of has reached its highest level in ten years, leading to doubling – and sometimes more – fuel prices in most African countries.

Evolution of the price of Brent since 2020 ($/bl)

Source : Energy Information Agency (EIA, USA), in https://tradingeconomics.com/commodity/brent-crude-oil

The situation in Africa

Africa's economic prospects were already not favorable before the invasion. Africa remains highly exposed to the pandemic and according to the World Bank (2022), per capita income in most African countries will remain below pre-pandemic levels at least until 2023. Median inflation has been announced to 5.1% year-on-year at the end of 2021. Africa, in particular Northern Africa, is, moreover, particularly affected by the rise in food prices, which represent nearly 40% of the budget of the households in many countries. Populations living below the poverty line (measured at $1.90 a day) have risen from 34% before the pandemic to 39% (The World Bank: African Economic Outlook 2021).

The rise in oil prices: a windfall effect for a limited number of producing countries…

Of the 54 African countries (of which, 49 in Sub-Saharan Africa), 12 are net exporters of oil and/or gas, plus South Africa for coal. In 2019 (The last pre-pandemic year), African oil countries produced 402 million tons (Mt) of crude, of which 78% (315 Mt) were exported. The 10 exporting countries of Sub-Saharan Africa represent 60% of production but a much higher proportion of exports (91%), due to the fact that North African countries spare a larger share of their production for their domestic market.

Larger oil exporters have already reaped substantial benefits from soaring prices. Angola's exports would represent, in pre-pandemic times, 36.5% of its GDP, 18.9% for Algeria and 10.3% for Nigeria. A study by the Policy Center for the New South, based in Rabat, estimated in a February 2022 note that a 20 to 30% increase in oil and gas prices, corresponding to what was observed before the outbreak of the war in Ukraine, would lead, if it continued, to an increase of 4 to 6% in the national income of a major exporting country, such as Algeria. If the conflict were to continue, and in the absence of measures intended to curb prices (e.g. temporary increase in production, access to strategic storage), the surplus revenue could more than offset the increase in the cost of certain basic foodstuffs such as wheat.

The table below shows, for a selection of African oil exporting countries, the additional revenue that would be generated in 2022 compared to 2021, if the price of a barrel were to remain in 2022 at the average price observed between February and March 2022 ($107, 0/bl). The difference with the average price for 2021 ($70.7/bl) is $36.3/bl), i.e. +51.3%.

|

Countries |

Exportations (ref. 2019) |

Estim’d additional revenue |

Countries |

Exportations (ref. 2019) |

Estim’d additional revenue |

|

|

Millions tons |

Billions USD |

|

Millions tons |

Billions USD |

|

Large-scale exporters |

Mid-scale exporters |

||||

|

Nigeria |

98,6 |

26,1 |

Gabon |

10,3 |

2,7 |

|

Angola |

62,4 |

16,5 |

Ghana |

10,1 |

2,7 |

|

Libye |

53,2 |

14,1 |

Sud-Soudan |

8,5 |

2,3 |

|

Algérie |

26,5 |

7,0 |

Guinée-Eq. |

8,0 |

2,1 |

…but a negative impact for the vast majority

The majority of African countries are net importers of energy, or, for a few, in quasi-self-sufficiency. First and foremost, the 42 net importing countries suffer directly from the increase in the price of crude oil (when they operate a refinery) or that of refined products (when they either do not operate a refinery, or they import additional product volumes to compensate for the insufficient capacity of their refining facilities).

Direct effects

The first and most visible impact is the increase in fuel costs at end-user’s level. The increase is all the greater when pump prices are little or not subsidized. However, even in some countries that have implemented a subsidies policy, the pressure on prices is becoming such that the subsidies mechanisms can no longer cover the gap between real costs and subsidised prices. In Nigeria, where a liter of subsidised gasoline is set at 165 naira (0.40 euros), pump stations have the greatest difficulty in meeting demand and waiting times to fill a car tank can last several hours . As for the price of diesel, considered unsubsidised, which is usually around 225 naira per liter (0.50 euro), it doubled and then tripled within a month, approaching 800 naira (1.78 euro) on March 18 .

The rise in the price of diesel oil particularly affects businesses and industries, not to mention private residences, which use backup generators to compensate for the shortcomings of the central electricity production system. Many businesses that use diesel generators have had to slow down or even shut down their operations, or reduce work hours to save on air conditioning. The impact is also critical on essential routine activities, such as the supply of drinking water in urban areas. A restaurateur notes that, at the public well that supplies his business in a suburb of Lagos, the price of twelve cans of water has risen in three months from 300 naira to nearly 1,000 naira.

Indirect effects

In addition to the direct or quasi-direct effects, the rise in prices indirectly increases the production costs of a large number of goods and services. First, because of the increase in the cost of transporting people and goods.

Then certain sectors are directly affected, in particular that of fertilizers, which are energy-intensive products. The most common, urea, is affected by the parallel rise in the price of natural gas. In mid-March in Kenya, a 50 kg bag of fertilizer would cost 6,500 shillings (52 euros) against 4,000 shillings (32 euros) a few months earlier, an increase of 60%.

The effects of the war at the sectoral level on Africa will most likely be amplified by the effect of deteriorating macroeconomic conditions in many states. The subsidies policies for certain energy products, in place in most African countries and already difficult to support in many of them, are emptying the coffers of the States. According to the World Bank, the cost of fuel subsidies was already equivalent to 2% of Nigerian GDP in 2021 – before the price hike.

In Tunisia, the State budget for 2022, prepared in the fall of 2021, was logically established on the basis of a barrel at $75. The rise in international prices has already created an additional charge for the compensation fund of around 7 bn dinars ($2.3 bn). This additional burden, which is likely to increase in the medium term, will directly affect the State budget, which will be forced to increase pump prices. And the Arab Institute of Business Leaders (IACE) estimates that the Tunisian authorities will have to speed up negotiations with the World Bank and the IMF to obtain exceptional emergency aid, which could reach $1 to $1.5 bn for the year 2022.

In addition to the rise in oil prices, the rise of policy rates intended to fight against inflation, the depreciation of certain risky assets due to the persistence of uncertainty, and the slowdown in European economies, will necessarily have repercussions on Africa. African countries that have access to international markets could see their borrowing costs increase by several percentage points, or even become inaccessible. This should not pose a major problem for some countries with low external debt and manageable current account deficits, such as Morocco. By contrast, many countries in Africa, especially those dependent on international assistance, have already reached high levels of external debt in the wake of the pandemic and are now particularly exposed.

Finally, we must underline the possible consequences at the geopolitical level. The increase in energy, which is not solely due to the war in Ukraine, is coupled with a surge in the prices of many basic food products, first and foremost cereals, which is a direct result of the conflict, as well as sugar, corn and cooking oils. While African households can spend up to two-thirds of their income on food, the caveats are mounting.

The Director of the IMF's Africa Department, Abebe Aemro Selassie, fears that “this new crisis can be read not only in the GDP figures, but in the exchange rates, the trade balances of States, inflation, and, consequently, through the frustration of the populations”.

Food Security

The main concern is the continent's food security. Russia and Ukraine are major wheat suppliers and fears of shortages have caused prices to soar since the start of the conflict. North Africa but also other countries in Sub-Saharan Africa, such as Kenya, are particularly exposed due to their dependence on imports. Egypt, where bread is an essential component of the diet of the poorest segments of the population, imports more than half of the wheat it consumes. And about 80% of these purchases used to come from the two belligerent countries.

In Sudan, which also depends on Russia and Ukraine for more than a third of its wheat supplies, nearly half of its 44 million people will go hungry this year, according to World Food Program predictions. The risks are also considered very alarming in all Sahelian countries, where there is already a serious food crisis.

"The war in Ukraine means hunger in Africa," IMF Managing Director Kristalina Georgieva warned on March 13, while Carmen Reinhart, the World Bank's lead economist, expressed on March 9 her "concerns for food security" and "risks of social unrest". The risks are considered particularly high in West Africa, where the economic context is very degraded. A food crisis on a scale unprecedented in ten years is already here: 26 million people are in a food emergency and need assistance, according to assessments by United Nations agencies established at the end of 2021 for 19 countries, within an area stretching from Senegal to the Central African Republic. A figure that experts project at 38 million by the summer, when the populations, mostly rural, will have to go through the lean season while the granaries will be empty.

The index of international prices of products imported by the countries of the West African Monetary Union (WAMU) has already recorded in January 2022 an increase of 26.4% over the previous year. Sign of their feverishness in the face of this price spiral, Burkina Faso, Chad and Côte d'Ivoire have decided to restrict exports of several commodities – thus aggravating the situation of their neighbours.

In this context, the war in Ukraine and Russia's decision to suspend its agricultural exports until the end of the year herald additional difficulties. Five countries – Mauritania, Mali, Senegal, Cameroon and Benin – are highly dependent on these two suppliers for their wheat supplies: 100% in the case of Mauritania, 60% for Senegal or Cameroon. “The quantities involved are not necessarily considerable, but in cities, wheat flour is used to make the bread and pancakes that the poorest people eat,” explains Ollo Sib, head of evaluations for the World Food Program (WFP) for West and Central Africa: “They risk being deprived of what is today the most accessible food.”

Henri Beaussant

ADEA